I was trying to understand the impact of the time dimension as a proxy for widespread credit crisis from 2006-2010. Did municipal bond behavior change as a result of the widespread financial market collapse? I figured that any impact would be manifest in the yearly issuance of debt -a statistically valid relationship between any of the year variables would show whether there was an impact in that year.

I obtained a bunch of municipal data – aggregated at the state level (strike 1) – to approach the kitchen sink model of predicting bond issuance behavior of municipalities. I took the log of each variable to determine elasticity, assigned dummy variables for each year, and put it into this first pooled OLS. It includes all of the data from 2006 to 2010:

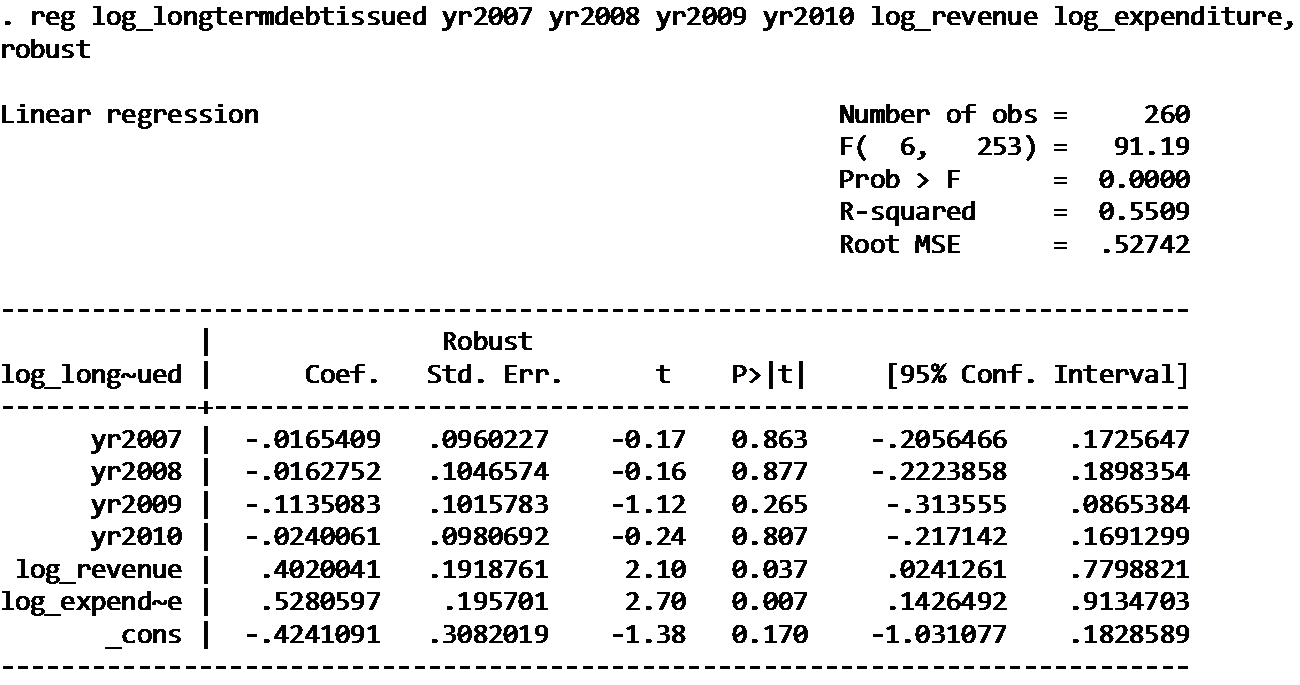

reg log_longtermdebtissued yr2007 yr2008 yr2009 yr2010 log_revenue log_expenditure, robust

This naive regression shows no evidence for a causal relationship between the time variables, while it shows a statistical and interesting relationship between the incidence of long-term debt issuance and revenue and expenditures. Interpretation of this model suggests that increased revenue leads to increased long-term debt issuance, and that increased expenses are not only associated with higher debt issuance, but at a greater rate than revenues.

xtreg log_longtermdebtissued yr2007 yr2008 yr2009 yr2010 log_revenue log_expenditure, fe robust

Building on the naive P-OLS regression, we now use fixed effects to account for the non-normal behavior of municipal debt-takers within each state. This fixed effect, robust to heteroskedasticity, provides further evidence for the importance of revenue and expenditures, and again leads us away from assigning causality to the interesting policy variables – the time dummies.

xtreg log_longtermdebtissued yr2007 yr2008 yr2009 yr2010 log_revenue log_expenditure lag_log_issue, fe robust

This last regression includes a lag variable of last year’s debt-issuance to account for any effect of the previous year’s debt issuance. Again, revenue and expenditures affect the bond-letting behavior. It is interesting that the lag variable is significant and has a negative impact. This means that higher debt-issuance in the previous year has a negative impact on the current year’s issuance of debt. Perhaps these are large, one-time projects or expenses, or that local leaders become debt-averse at certain debt levels. Further analysis of outstanding debt levels as they relate to the issuance of bond debt would help to tease out the tipping point for this possible aversion to debt.

Also, it is interesting to note that although the year 2009 is still not significant, it is far less insignificant than the others. This may mean that, for some states, municipal debt was affected by the time variable (2009). I’m not sure how to tease out that impact but it would be cool!

Below is my STATA dataset. It’s a mess, but I’m new at this.

Stata .dta dataset – Municipal debt statistics by state from 2006-2010